Advertisements

Cosigning Loan Risks Explained: What I Wish Someone Had Told Me Before I Signed

Here’s a stat that still makes my stomach drop — according to a CreditKarma survey, 38% of cosigners ended up paying part or all of the loan themselves. I know that number is real because I lived it. A few years back, my cousin asked me to cosign an auto loan, and let me tell you, that decision haunted my finances for longer than I’d like to admit!

Understanding cosigning loan risks is one of those things that nobody really teaches you. It sounds simple enough — you’re just helping someone out, right? But the reality is way more complicated, and I want to walk you through what can actually go wrong so you don’t learn the hard way like I did.

What Does Cosigning a Loan Actually Mean?

When you cosign a loan, you’re basically telling the lender, “Hey, if this person can’t pay, I’ve got it covered.” You become equally responsible for the full debt. That’s not a small thing.

The borrower usually needs a cosigner because their credit score is too low or they don’t have enough income to qualify alone. So right from the start, you’re vouching for someone the bank already considers a risk. That should tell you something, honestly.

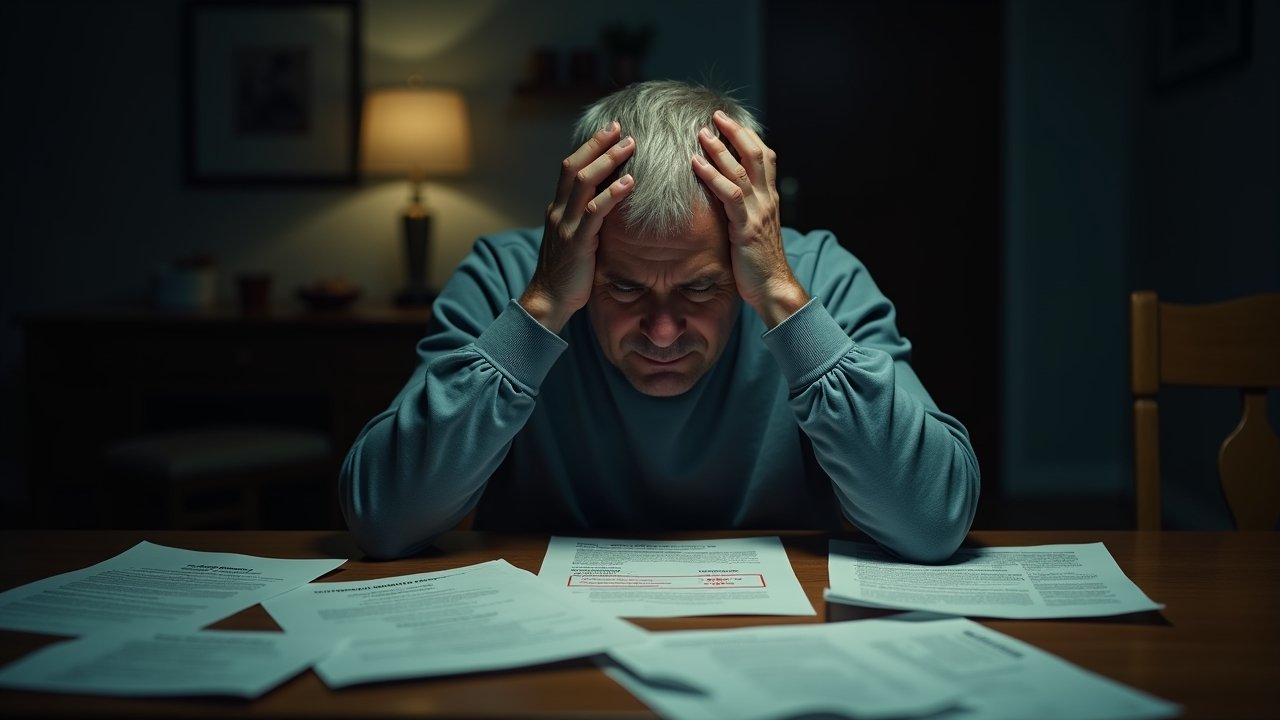

Your Credit Score Is on the Line

This one bit me hard. When my cousin missed a couple payments — he swore he’d “get caught up next month” — my credit score took a nosedive. The loan shows up on both your credit reports, and any late payment or default gets reported for you too.

Even if payments are made on time, that cosigned loan increases your debt-to-income ratio. So when I tried to refinance my mortgage a year later, the lender looked at me like I was crazy. I had this whole other loan sitting on my record that technically wasn’t even mine.

You Could Get Stuck Paying the Entire Balance

This is the big one that people don’t fully grasp. If the primary borrower stops paying, the lender doesn’t care about your relationship or who was “supposed to” make payments. They come after you for every single penny.

And it’s not just the remaining balance. We’re talking late fees, collection costs, and sometimes even legal fees piled on top. The FTC warns that cosigners could owe up to the full amount of the debt, including these extra charges.

It Can Wreck Relationships (Ask Me How I Know)

Look, money and family don’t mix well. Period. When I started getting collection calls about my cousin’s car loan, things got real awkward at Thanksgiving dinner.

I was frustrated — honestly, I was furious. He kept dodging my texts about payments while posting vacation photos on Instagram. The resentment builds up fast when you’re watching your own financial health deteriorate because of someone else’s choices. We barely talked for two years after that whole mess.

Practical Tips If You’re Considering Cosigning

Alright, so maybe you still want to help someone out. I get it. Here’s what I’d recommend based on my experience:

- Set up payment alerts — Make sure you have access to the loan account so you know immediately if a payment is missed.

- Have an honest conversation — Talk about what happens if they can’t pay. Get it in writing if you can.

- Ask about cosigner release — Some lenders will remove the cosigner after a certain number of on-time payments. Always ask about this upfront.

- Only cosign what you can afford to pay — Because there’s a real chance you might have to.

- Consider alternatives — Maybe you could help them build credit another way, like adding them as an authorized user on a credit card instead.

Before You Pick Up That Pen

Advertisements

Cosigning a loan is one of the most generous — and most dangerous — financial favors you can do for someone. Your credit, your wallet, and even your relationships are all at stake. I’m not saying never do it, but please go in with your eyes wide open.

Every situation is different, so take the time to evaluate yours carefully. Think about your own financial goals before putting them at risk for someone else’s. And if you want to keep learning about smart money moves and avoiding financial pitfalls, make sure you check out more posts on Dollar Docket — we’re all about helping you protect your hard-earned cash!