The Income-Based Budgeting Method: How I Finally Stopped Fighting With My Money

Advertisements

Here’s a stat that honestly shook me — nearly 78% of Americans live paycheck to paycheck. I was one of them for years. Then I stumbled onto the income-based budgeting method, and it genuinely changed the whole game for me.

Look, I’m not gonna pretend I’m some financial guru. I’m a regular person who was tired of wondering where my money went every single month. If that sounds familiar, stick around — because this approach might be exactly what you need too!

So What Exactly Is Income-Based Budgeting?

An income-based budgeting method is exactly what it sounds like — you build your entire budget around your actual take-home pay. Not what you wish you made, not your gross salary, but the real dollars hitting your bank account. Every expense, every savings goal, every little splurge gets allocated from that number.

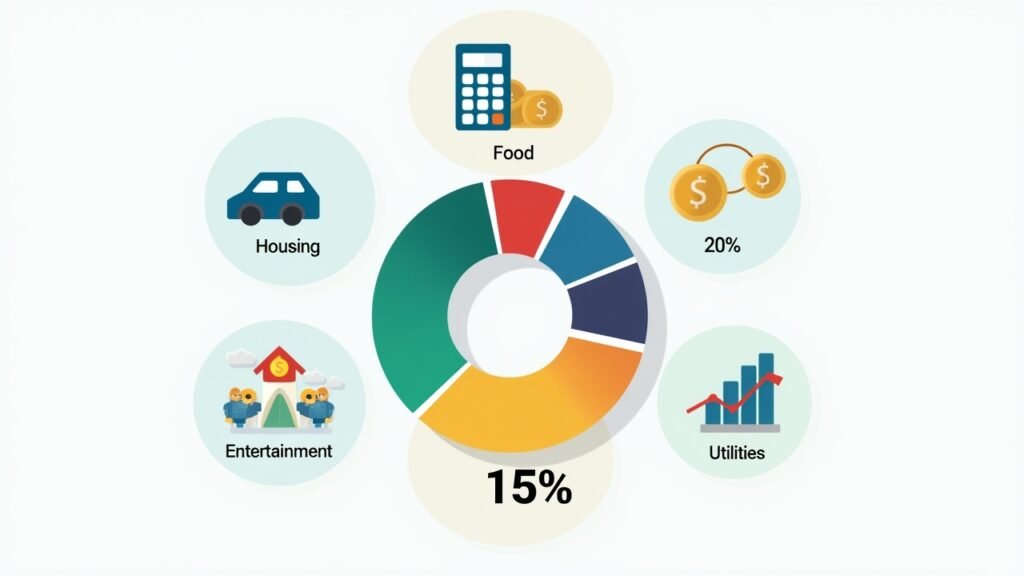

The beauty here is simplicity. Instead of tracking every latte like some obsessive accountant, you’re creating spending categories based on percentages of your income. A lot of people confuse this with the 50/30/20 rule, and honestly, that’s a great starting framework — 50% needs, 30% wants, 20% savings.

My Embarrassing Wake-Up Call

I’ll never forget the month I overdrafted three times in one week. Three times! I was making decent money as a teacher, but my budget was based on vibes, not actual numbers.

My mistake was building a budget around what I thought I should spend rather than what I actually earned after taxes and deductions. Once I sat down and looked at my real net income — which was way less than I assumed — everything clicked. It was humbling, but man, it was necessary.

How to Set Up Your Own Income-Based Budget

Alright, here’s where we get practical. I’ve been tweaking my personal finance strategy for about five years now, and this is the process that actually works.

- Calculate your true net income. Add up every paycheck, side hustle, and regular deposit you receive monthly. If your income varies, use the average of your last three months.

- List your fixed expenses first. Rent, car payment, insurance, subscriptions — anything that’s the same every month gets written down immediately.

- Assign percentages to variable categories. Groceries, gas, entertainment, dining out. This is where most people mess up because they underestimate these costs.

- Build in a savings allocation. Even if it’s just 10% to start, pay yourself first. I use an automatic transfer so I never “forget.”

- Leave a buffer. I learned this the hard way — always keep about 5% unallocated for those random expenses that pop up.

Tools That Actually Help

I tried spreadsheets, notebooks, even a whiteboard on my fridge once. What finally stuck was using a budgeting app like YNAB (You Need A Budget) because it’s literally designed around this zero-based, income-first philosophy. It’s not free, but it paid for itself within the first month.

That said, a simple Google Sheet works fine too. The tool matters way less than the habit of actually checking in with your budget weekly.

Common Mistakes I’ve Seen (and Made)

The biggest trap? Being too aggressive with your savings goals right out the gate. I once tried allocating 40% to savings and debt payoff, and by week two I was so miserable I abandoned the whole budget. Sustainable money management beats perfection every time.

Another thing — don’t forget irregular expenses. Car registration, annual subscriptions, holiday gifts. These sneak up on you if they aren’t baked into your monthly budget as small recurring amounts. Trust me on this one.

Your Money, Your Rules

The income-based budgeting method isn’t about restriction — it’s about giving every dollar a job so you’re not stressed at the end of the month. It was honestly the first budget approach that didn’t make me feel like I was being punished for spending money.

Advertisements

Remember, your budget should fit your life, not the other way around. Tweak the percentages, adjust the categories, and give yourself grace when things don’t go perfectly. The important thing is you’re being intentional with your money.

If you found this helpful, there’s plenty more where it came from — head over to the Dollar Docket blog for more practical tips on budgeting, saving, and building a financial life that actually feels good. You got this!